Financing major expenses without overextending requires a careful balance of credit use, cash flow awareness, and risk management. By understanding borrowing costs, aligning repayments with income stability, and maintaining liquidity, individuals can make informed financial decisions. This guide outlines practical strategies, real-world examples, and expert-backed insights to help Americans finance responsibly while protecting long-term financial health.

Understanding What “Overextending” Really Means

Overextending financially isn’t just about taking on too much debt—it’s about misaligning your obligations with your income, savings, and risk tolerance. In the U.S., where access to credit is relatively easy, many households find themselves stretched not because of reckless spending, but because of poor structuring of otherwise reasonable financial decisions.

At its core, overextension happens when your financial commitments begin to limit your flexibility. This could mean struggling to cover monthly bills, delaying savings, or relying on additional debt to stay afloat. According to the Federal Reserve, the average American household carries thousands in revolving credit card debt, often at interest rates exceeding 20%, making even small miscalculations costly over time.

The Three Pillars of Sustainable Financing

A balanced financing strategy rests on three interconnected pillars: credit, cash flow, and risk. Ignoring any one of these can lead to long-term financial strain.

1. Credit: Use It Strategically, Not Conveniently

Credit is a tool, not a fallback. The goal isn’t to avoid it entirely, but to use it with intention.

For example, financing a car with a low-interest auto loan may be more efficient than paying entirely in cash—especially if that cash can remain invested or serve as an emergency buffer. However, using high-interest credit cards for recurring expenses without a repayment plan quickly leads to compounding debt.

Key considerations include:

- Interest rates and total borrowing costs

- Loan terms and repayment flexibility

- Impact on your credit score and future borrowing ability

A good rule of thumb: if you cannot clearly outline how and when a debt will be repaid, it’s likely not the right financing choice.

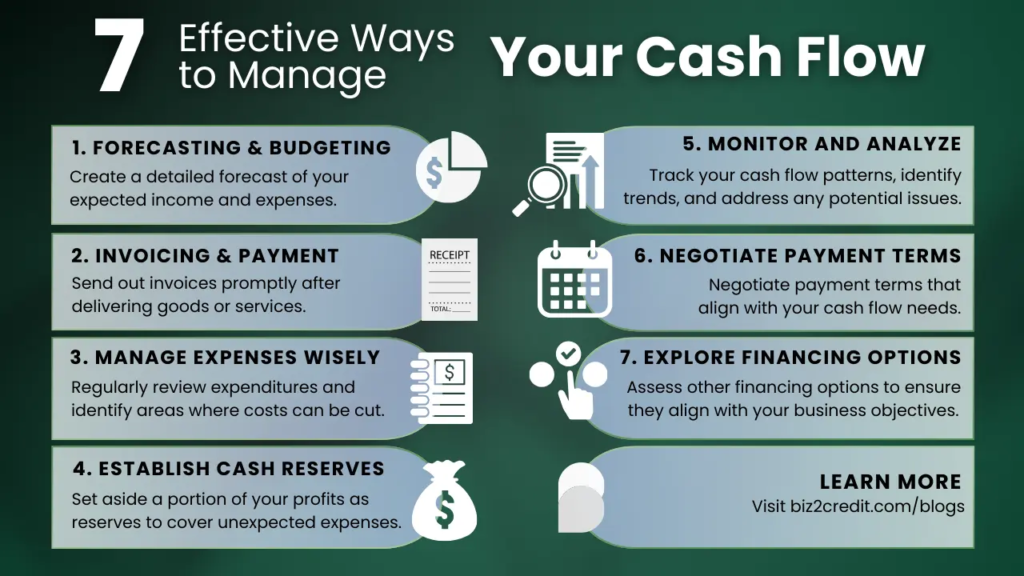

2. Cash Flow: The Foundation of Financial Stability

Cash flow—the timing and consistency of income versus expenses—is often overlooked in financing decisions. Yet it is the most immediate indicator of whether a financial commitment is sustainable.

Consider two individuals with identical salaries:

- One has stable, predictable income and minimal fixed expenses

- The other has variable income and high recurring obligations

The same loan may be manageable for one and risky for the other.

To maintain healthy cash flow:

- Keep fixed obligations (housing, debt payments) below 50% of income

- Build a buffer for irregular expenses

- Regularly review monthly inflows and outflows

A practical example: If your monthly take-home pay is $5,000, and your fixed costs already total $2,500, adding a $600 loan payment may push your finances into a fragile position—especially if unexpected expenses arise.

3. Risk: Preparing for the Unknown

Risk in personal finance is often underestimated. Job loss, medical expenses, or economic downturns can quickly turn manageable debt into a burden.

Mitigating risk involves:

- Maintaining an emergency fund (3–6 months of expenses)

- Avoiding over-reliance on variable income streams

- Diversifying financial commitments (not all tied to one asset or liability)

For instance, financing a home at the upper limit of your budget may seem feasible today, but leaves little room for future uncertainty such as rising property taxes or maintenance costs.

How to Evaluate a Financing Decision Before You Commit

Before taking on any new financial obligation, it’s critical to evaluate not just affordability, but resilience.

Ask yourself:

- Can I comfortably make this payment even if my income drops by 10–20%?

- How will this affect my ability to save or invest?

- What is the total cost of borrowing, not just the monthly payment?

- Am I choosing this option out of necessity or convenience?

A structured approach can help:

- Calculate your debt-to-income (DTI) ratio

- Stress-test your budget under different scenarios

- Compare multiple financing options (loans, leases, cash purchases)

- Factor in hidden costs such as fees, insurance, or maintenance

Common Financing Mistakes—and How to Avoid Them

Even financially disciplined individuals can fall into common traps when managing credit and cash flow.

1. Focusing Only on Monthly Payments

Low monthly payments often mask longer loan terms and higher total interest costs. Always evaluate the full repayment amount.

2. Ignoring Variable Interest Rates

Adjustable-rate loans can become significantly more expensive over time, especially in rising interest rate environments.

3. Overestimating Future Income

Promotions, bonuses, or business growth are not guaranteed. Base decisions on current, reliable income.

4. Underestimating Lifestyle Inflation

As income increases, so do expenses. Without discipline, higher earnings don’t necessarily translate to better financial stability.

Practical Strategies to Stay Financially Balanced

Balancing credit, cash flow, and risk requires ongoing attention rather than one-time decisions.

Adopt a Layered Financing Approach

Instead of relying on a single funding source, combine:

- Cash savings for partial payments

- Low-interest loans for larger expenses

- Minimal use of high-interest credit

Prioritize Liquidity Over Ownership

Maintaining accessible cash reserves often provides more long-term security than fully owning depreciating assets.

Automate and Monitor Payments

Automating payments reduces missed deadlines, but regular monitoring ensures you remain aware of your financial position.

Refinance When Appropriate

If interest rates drop or your credit improves, refinancing can reduce costs—but only if fees and terms justify the change.

Real-World Example: Financing a Home Without Overstretching

Consider a household earning $90,000 annually. They qualify for a mortgage that would consume 40% of their gross income. While technically approved, this level leaves little room for savings or unexpected costs.

Instead, they choose a home priced 15% lower, reducing their monthly payment and allowing them to:

- Maintain a six-month emergency fund

- Continue retirement contributions

- Absorb maintenance costs without additional debt

Over time, this approach provides greater financial stability, even if it means compromising slightly on property size or location.

The Role of Financial Discipline and Awareness

Financial tools and strategies are only effective when paired with consistent discipline. Regularly reviewing your financial position—monthly or quarterly—helps ensure that your decisions remain aligned with your goals.

Technology can assist, but judgment remains essential. Budgeting apps, credit monitoring tools, and financial dashboards provide data, but interpreting that data correctly is what prevents overextension.

Frequently Asked Questions

1. What is a safe debt-to-income ratio?

Most financial experts recommend keeping your DTI below 36%, though some lenders allow higher thresholds.

2. How much emergency savings should I have?

Typically, 3–6 months of living expenses, depending on job stability and income variability.

3. Is it better to pay cash or finance large purchases?

It depends on interest rates, liquidity needs, and opportunity cost. Low-interest financing can be beneficial if cash reserves remain intact.

4. How can I reduce financial risk when borrowing?

Maintain savings, avoid variable-rate loans when possible, and ensure payments fit comfortably within your budget.

5. Are credit cards always a bad financing option?

Not necessarily, but they should be used for short-term borrowing and paid off quickly to avoid high interest.

6. What’s the biggest mistake people make with loans?

Focusing on monthly payments instead of total borrowing cost.

7. How often should I review my finances?

At least monthly, with a more detailed review quarterly.

8. Can refinancing always save money?

No, it depends on fees, interest rates, and remaining loan terms.

9. Should I avoid all debt to stay safe?

Not necessarily. Strategic debt can support long-term goals if managed responsibly.

10. How do I know if I’m overextended?

If you struggle to save, rely on credit for essentials, or feel financially stressed, you may be overextended.

A Sustainable Path Forward in Everyday Financing

Financial stability is rarely about avoiding debt entirely—it’s about managing it intelligently within the broader context of your life. By aligning borrowing decisions with cash flow realities and preparing for uncertainty, you create a system that supports both present needs and future goals. The most effective financial strategies are those that remain resilient under pressure, not just optimal under ideal conditions.

Key Insights at a Glance

- Balance credit use with realistic income expectations

- Prioritize consistent cash flow over aggressive borrowing

- Maintain emergency savings to reduce financial risk

- Evaluate total borrowing costs, not just monthly payments

- Avoid decisions based on uncertain future income

- Use debt strategically, not reactively

- Regularly review and adjust your financial plan